All Categories

Featured

Table of Contents

- – What is Term Life Insurance For Seniors? How I...

- – Why Level Term Life Insurance Meaning Matters

- – What is Level Benefit Term Life Insurance? A ...

- – All About Direct Term Life Insurance Meaning ...

- – What is Joint Term Life Insurance? Key Consi...

- – What Makes Term Life Insurance For Spouse St...

If George is detected with a terminal ailment during the first policy term, he most likely will not be qualified to renew the policy when it ends. Some plans provide guaranteed re-insurability (without evidence of insurability), yet such functions come with a greater price. There are a number of types of term life insurance.

Usually, most companies provide terms varying from 10 to thirty years, although a couple of offer 35- and 40-year terms. Level-premium insurance coverage has a fixed monthly repayment for the life of the policy. A lot of term life insurance coverage has a degree premium, and it's the kind we have actually been referring to in many of this short article.

Term life insurance policy is eye-catching to youngsters with children. Parents can get considerable protection for an affordable, and if the insured dies while the plan is in effect, the family members can count on the fatality benefit to change lost revenue. These plans are also fit for people with growing families.

What is Term Life Insurance For Seniors? How It Works and Why It Matters?

Term life plans are excellent for people who desire considerable protection at a reduced expense. People who possess entire life insurance policy pay more in premiums for much less protection but have the safety of recognizing they are secured for life.

The conversion cyclist ought to permit you to convert to any kind of long-term policy the insurance provider supplies without restrictions. The key attributes of the biker are maintaining the original health ranking of the term plan upon conversion (also if you later have health and wellness problems or end up being uninsurable) and determining when and just how much of the protection to convert.

Of program, total premiums will certainly raise considerably because entire life insurance coverage is a lot more costly than term life insurance policy. Medical conditions that create during the term life duration can not cause costs to be increased.

Why Level Term Life Insurance Meaning Matters

Whole life insurance coverage comes with substantially greater monthly costs. It is indicated to supply coverage for as lengthy as you live.

It depends upon their age. Insurance coverage firms established an optimum age limit for term life insurance policy policies. This is normally 80 to 90 years of ages however might be greater or reduced relying on the firm. The costs likewise climbs with age, so a person matured 60 or 70 will pay significantly greater than someone decades more youthful.

Term life is rather comparable to cars and truck insurance. It's statistically unlikely that you'll need it, and the premiums are cash down the drainpipe if you do not. If the worst happens, your family members will get the advantages.

What is Level Benefit Term Life Insurance? A Beginner's Guide

For the a lot of part, there are 2 sorts of life insurance coverage plans - either term or permanent plans or some combination of the 2. Life insurance companies offer different forms of term plans and conventional life policies as well as "rate of interest sensitive" products which have actually become more widespread because the 1980's.

Term insurance offers defense for a specified time period. This duration might be as short as one year or offer coverage for a details variety of years such as 5, 10, two decades or to a specified age such as 80 or in some cases up to the earliest age in the life insurance policy mortality tables.

All About Direct Term Life Insurance Meaning Coverage

Currently term insurance coverage prices are very competitive and among the most affordable traditionally experienced. It must be noted that it is an extensively held idea that term insurance is the least pricey pure life insurance protection readily available. One needs to evaluate the plan terms meticulously to make a decision which term life options are ideal to meet your certain conditions.

With each new term the premium is increased. The right to renew the plan without proof of insurability is a crucial benefit to you. Otherwise, the threat you take is that your wellness might weaken and you might be incapable to obtain a policy at the exact same rates or perhaps at all, leaving you and your recipients without protection.

The size of the conversion period will certainly differ depending on the type of term plan bought. The premium price you pay on conversion is generally based on your "current obtained age", which is your age on the conversion date.

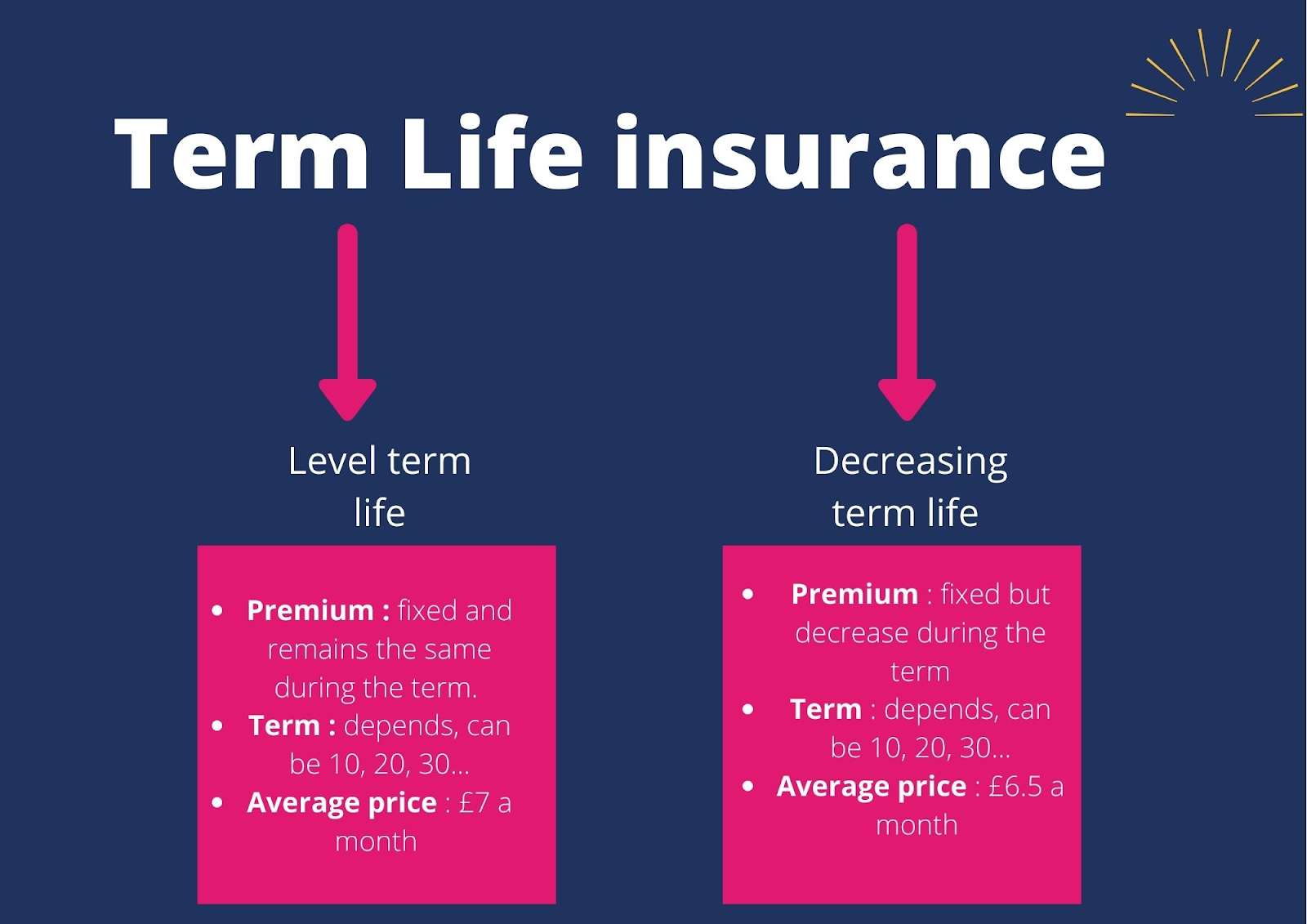

Under a level term policy the face quantity of the plan remains the same for the entire period. With decreasing term the face quantity reduces over the period. The costs remains the exact same each year. Commonly such policies are offered as home loan defense with the amount of insurance lowering as the equilibrium of the home mortgage decreases.

Traditionally, insurance firms have not can transform premiums after the policy is offered. Given that such plans might continue for several years, insurers have to make use of conservative mortality, rate of interest and expenditure price estimates in the premium estimation. Flexible premium insurance, however, enables insurance companies to provide insurance policy at reduced "current" premiums based upon less conservative presumptions with the right to transform these premiums in the future.

What is Joint Term Life Insurance? Key Considerations?

While term insurance is developed to provide defense for a defined amount of time, irreversible insurance policy is created to supply coverage for your entire lifetime. To maintain the costs price level, the costs at the younger ages surpasses the real price of protection. This added premium develops a get (cash value) which assists pay for the policy in later years as the expense of defense rises above the premium.

The insurance business invests the excess premium bucks This type of plan, which is in some cases called cash money worth life insurance coverage, creates a cost savings element. Cash money values are important to a permanent life insurance coverage plan.

Occasionally, there is no relationship between the dimension of the cash money value and the premiums paid. It is the cash worth of the policy that can be accessed while the insurance holder is active. The Commissioners 1980 Standard Ordinary Mortality Table (CSO) is the existing table utilized in determining minimal nonforfeiture values and plan reserves for normal life insurance coverage plans.

What Makes Term Life Insurance For Spouse Stand Out?

Lots of long-term plans will certainly include provisions, which define these tax requirements. There are 2 basic classifications of permanent insurance policy, conventional and interest-sensitive, each with a variety of variations. In addition, each group is normally readily available in either fixed-dollar or variable form. Traditional entire life policies are based upon lasting estimates of cost, interest and mortality.

{kind=link}

Table of Contents

- – What is Term Life Insurance For Seniors? How I...

- – Why Level Term Life Insurance Meaning Matters

- – What is Level Benefit Term Life Insurance? A ...

- – All About Direct Term Life Insurance Meaning ...

- – What is Joint Term Life Insurance? Key Consi...

- – What Makes Term Life Insurance For Spouse St...

Latest Posts

Senior Burial Insurance Program

United Final Expense Services Reviews

Final Expense Insurance License

More

Latest Posts

Senior Burial Insurance Program

United Final Expense Services Reviews

Final Expense Insurance License