All Categories

Featured

Table of Contents

That commonly makes them a more economical choice for life insurance policy coverage. Some term policies might not keep the costs and survivor benefit the same over time. You do not intend to erroneously assume you're acquiring level term coverage and afterwards have your death advantage modification in the future. Many individuals obtain life insurance policy protection to help monetarily secure their loved ones in instance of their unforeseen death.

Or you might have the choice to transform your existing term coverage right into a long-term plan that lasts the remainder of your life. Various life insurance policy plans have potential advantages and drawbacks, so it is essential to understand each before you choose to buy a policy. There are a number of advantages of term life insurance policy, making it a popular option for insurance coverage.

As long as you pay the costs, your beneficiaries will obtain the survivor benefit if you die while covered. That said, it's vital to keep in mind that most plans are contestable for two years which indicates protection could be retracted on death, must a misrepresentation be located in the application. Plans that are not contestable frequently have actually a graded death advantage.

Premiums are generally lower than whole life policies. With a level term plan, you can choose your insurance coverage amount and the plan length. You're not secured into a contract for the remainder of your life. Throughout your policy, you never have to worry regarding the premium or survivor benefit amounts altering.

And you can't pay out your policy during its term, so you won't receive any kind of financial gain from your previous insurance coverage. Similar to various other sorts of life insurance, the price of a level term plan depends on your age, coverage requirements, work, lifestyle and wellness. Generally, you'll discover a lot more economical insurance coverage if you're younger, healthier and less risky to guarantee.

Preferred A Renewable Term Life Insurance Policy Can Be Renewed

Given that degree term premiums stay the exact same throughout of coverage, you'll know specifically how much you'll pay each time. That can be a huge assistance when budgeting your costs. Level term insurance coverage also has some versatility, enabling you to personalize your policy with added functions. These frequently can be found in the kind of riders.

You may have to meet certain conditions and certifications for your insurer to pass this motorcyclist. There also might be an age or time limit on the insurance coverage.

The survivor benefit is commonly smaller sized, and coverage generally lasts up until your kid transforms 18 or 25. This rider may be a much more economical method to help ensure your children are covered as bikers can typically cover numerous dependents at when. As soon as your kid ages out of this insurance coverage, it may be feasible to transform the cyclist right into a brand-new policy.

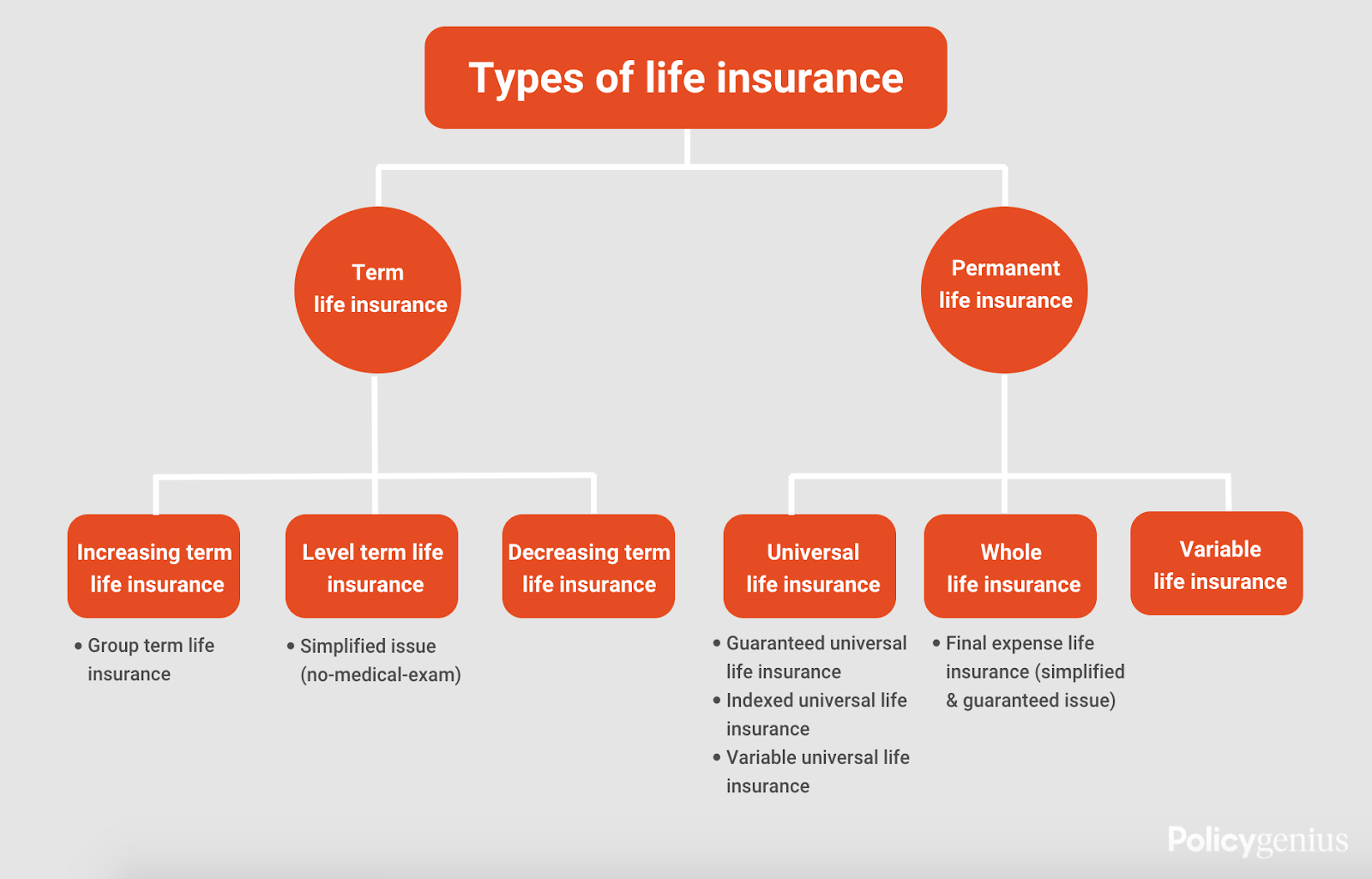

When comparing term versus permanent life insurance policy. joint term life insurance, it's important to keep in mind there are a few various types. One of the most usual kind of permanent life insurance coverage is entire life insurance coverage, yet it has some key distinctions contrasted to level term insurance coverage. Here's a basic summary of what to consider when comparing term vs.

Whole life insurance policy lasts for life, while term insurance coverage lasts for a certain duration. The costs for term life insurance policy are generally less than whole life coverage. However, with both, the costs continue to be the very same throughout of the plan. Whole life insurance policy has a cash money worth element, where a portion of the costs may expand tax-deferred for future demands.

One of the main functions of degree term protection is that your costs and your fatality benefit do not transform. You might have coverage that begins with a death advantage of $10,000, which can cover a mortgage, and then each year, the death benefit will lower by a set amount or portion.

As a result of this, it's usually a much more inexpensive type of level term protection. You may have life insurance coverage with your company, however it might not be enough life insurance policy for your requirements. The very first step when buying a plan is identifying just how much life insurance policy you need. Think about variables such as: Age Family members size and ages Employment standing Revenue Financial debt Way of life Expected last costs A life insurance policy calculator can assist figure out just how much you require to start.

After picking a policy, complete the application. For the underwriting process, you might need to offer general individual, health, way of living and work info. Your insurance firm will identify if you are insurable and the risk you may provide to them, which is mirrored in your premium costs. If you're authorized, sign the paperwork and pay your first premium.

Budget-Friendly Short Term Life Insurance

You may want to update your beneficiary details if you've had any kind of considerable life adjustments, such as a marital relationship, birth or divorce. Life insurance policy can occasionally really feel complicated.

No, level term life insurance policy does not have money value. Some life insurance coverage plans have an investment feature that allows you to build cash worth with time. A part of your costs payments is reserved and can gain passion in time, which grows tax-deferred during the life of your protection.

You have some options if you still desire some life insurance policy coverage. You can: If you're 65 and your protection has run out, for instance, you may want to get a new 10-year degree term life insurance plan.

Effective Level Premium Term Life Insurance Policies

You might be able to transform your term coverage right into an entire life plan that will last for the rest of your life. Numerous kinds of degree term policies are convertible. That indicates, at the end of your insurance coverage, you can transform some or every one of your plan to whole life insurance coverage.

Degree term life insurance is a plan that lasts a collection term normally in between 10 and 30 years and comes with a level survivor benefit and level premiums that stay the very same for the entire time the policy holds. This indicates you'll know exactly how much your settlements are and when you'll need to make them, allowing you to budget as necessary.

Level term can be an excellent alternative if you're wanting to purchase life insurance policy coverage for the very first time. According to LIMRA's 2023 Insurance coverage Barometer Study, 30% of all adults in the U.S. requirement life insurance policy and do not have any sort of plan yet. Degree term life is foreseeable and budget friendly, that makes it among the most preferred kinds of life insurance policy.

{kind=link}

Latest Posts

Senior Burial Insurance Program

United Final Expense Services Reviews

Final Expense Insurance License